Money myths that can burn a hole in your pocket, and how to spot them

There are several myths such as mutual funds with lower NAVs are cheaper, fixed-income investments are better than equity to plan for retirement and more.

The lack of adequate financial literacy creates fertile ground for the propagation and acceptance of financial myths. While the wide prevalence of these myths or misconceptions stop many consumers from making optimal financial decisions, falling for some of these can have long-term adverse consequences on their financial health.

Here are some of the top money myths that investors should avoid for their financial well-being.

Mutual funds with lower NAVs are cheaper

This has been around ever since the Indian mutual funds industry started to expand sometime in the 1990s. Many retail investors wrongly consider mutual funds (MFs) with lower net asset values (NAVs) to be cheaper. This misconception is often used by many to promote new fund offers (NFOs) as their units are issued at a face value of Rs 10.

However, multiple factors determine the NAV of any MF. For example, as the NAV of a fund is determined on the basis of the market value of its constituent investments, a well-managed fund’s NAV can grow faster than that of other funds, leading it to register a higher NAV over the period.

Similarly, newer MFs have lower NAVs compared to older ones as the former had less time to grow. Thus, using NAVs as the determining factor for fund selection may lead investors to end up with underperforming funds. Instead, MF investors should use the funds’ past performance, the suitability of those funds for achieving their financial goals as well as the future prospects of those funds in outperforming their benchmark indices and peer funds as the main selection parameters.

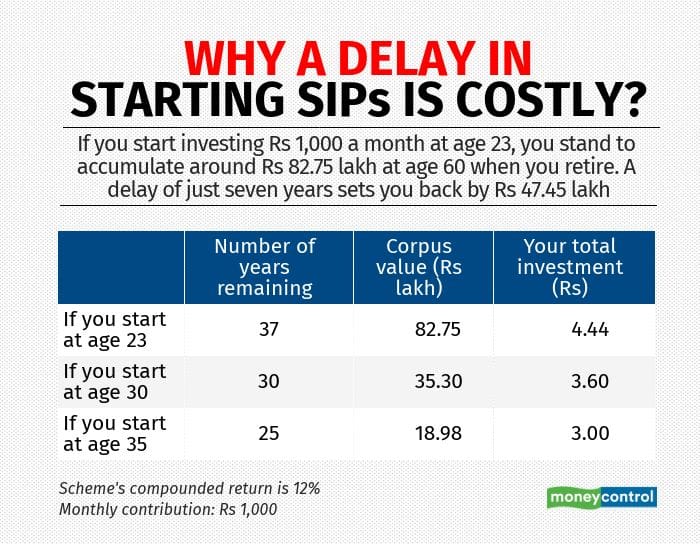

Are you young? Retirement planning can wait

Investors in their 30s and 40s often tend to put off their retirement planning for their later years. Instead, they prioritise other financial goals such as purchasing a car or home or saving for holidays. However, such individuals neglect the power of compounding.

The returns generated from their investment would start generating returns on their own, leading to bigger corpuses. For example, if a 30-year-old invests Rs 10,000 per month in equity funds through systematic investment plans (SIPs) for his or her retirement corpus, s/he would build a retirement corpus of Rs 3.49 crore by the time s/he turns 60, assuming an annualised return of 12 percent.

However, if they were to start investing for a retirement corpus from the age of 45, they would need a monthly investment of about Rs 70,000 to build the same corpus by the age of 60, assuming the same rate of returns. Thus, starting retirement investments earlier would allow one to create bigger corpus with much smaller contributions.

Mutual fund dividends are good

Many investors wrongly consider dividends declared by MFs as windfall income. This leads them to opt for the dividend option while investing in MFs. However, they fail to understand that dividends are paid out from the funds’ own assets under management (AUM), which means their investors’ own money. As a result, the dividend-declaring fund reduces its NAV by the dividend paid. Moreover, the dividend amount is calculated as a percentage of the fund’s face value and not on the NAV.

Moreover, the dividend option is also inefficient in terms of taxation as the earned dividends are taxed as per the tax slabs the investors fall in. Thus, investors should always opt for the growth option and, thereby, benefit from the power of compounding to generate a bigger corpus over a period of time.

I don’t have enough money to invest; it’s not worth it

Young investors, especially those in their 20s, and those with low savings rates tend to postpone their investments till they accumulate a sizeable corpus in their bank account. However, the minimum amount for lump-sum investment in most MF schemes is just Rs 5,000. Similarly, the minimum amount for an SIP and additional lump-sum investments are Rs 1,000 for most mutual fund schemes.

Many MF schemes offer lower minimum investment amounts. With such a low threshold, one does not need big-ticket savings to start investing in MFs. Instead, individuals with lower savings rates should start investing in MFs through the SIP mode and benefit from the power of compounding. As and when their incomes and saving rates increase, they should gradually increase the ticket size of their monthly SIPs.

Regular investment through the SIP mode would instil financial discipline, ensure rupee cost averaging by purchasing more units at lower NAVs during market corrections, and eliminate the need for timing investments and monitoring markets.

Fixed-income investments are better than equity to plan for retirement

Many investors tend to avoid equities while investing for their retirement corpus. They usually tend to invest in fixed income instruments like public provident fund, National Savings Certificate, bank/post office fixed deposits, Kisan Vikas Patra and endowment policies to create their retirement corpus. However, the returns generated by fixed-income instruments rarely beat inflation rates.

Moreover, creating post-retirement corpuses are long-term financial goals, preferably spanning decades. As the returns generated by equities beats the fixed-income asset class and inflation over the long term by a wide margin, equity is the most appropriate asset class for creating a post-retirement corpus.

Thus, investment contributions to a retirement corpus should always be equity-heavy. Once an investor is two or three years from retirement age, s/he can steadily shift to fixed-income instruments depending on risk appetite, post-retirement expenses, etc.Source / Credits / Reference: Money ControlRef URL: https://bit.ly/3T9nHof

Back to blogs

Blog Views : 555 01-04-2025