When people think about financial planning, they often imagine strict budgets, endless restrictions, and saying “no” to everything enjoyable. But true financial success is not built only on discipline—it is built on balance.

Just like a healthy lifestyle needs both exercise and rest, a healthy financial life needs financial resolutions for flexibility and financial obligations for discipline.

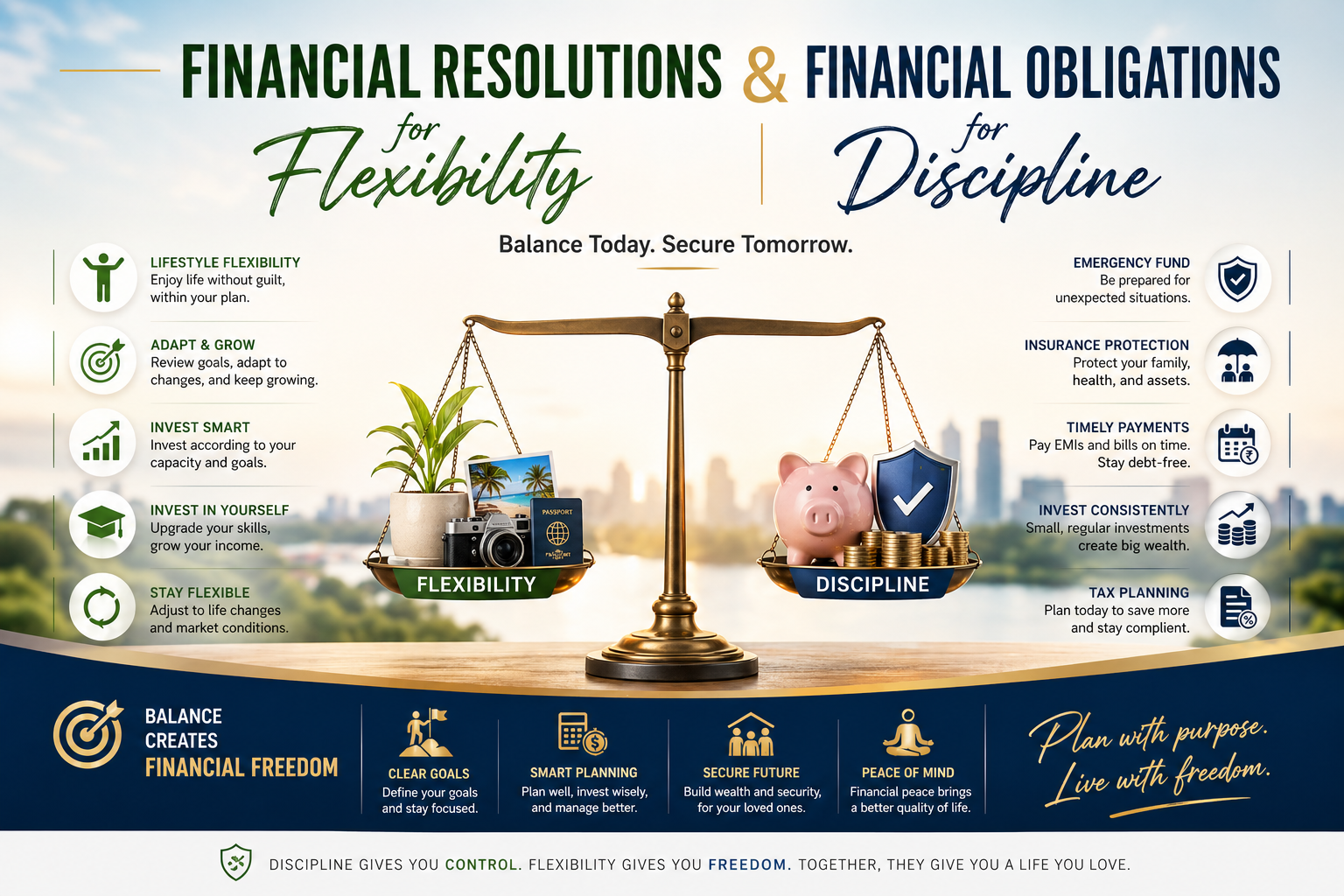

If you only focus on discipline, life feels stressful. If you only focus on flexibility, money slips away. The smartest approach is to combine both.

What Are Financial Resolutions for Flexibility?

Financial resolutions are personal commitments that allow room for enjoyment, adaptation, and changing life situations. They are not rigid rules they are smart promises to yourself.

Examples include:

1. Keep a Lifestyle Buffer

Set aside a small monthly amount for leisure, travel, dining out, or hobbies. This prevents guilt spending and helps maintain balance.

2. Review Goals Every 6 Months

Life changes—income changes, family needs evolve, opportunities arise. Flexible planning means reviewing goals regularly rather than blindly following old plans.

3. Invest According to Current Capacity

Some months you may invest more, some months less. What matters is consistency over perfection.

4. Allow for Career Growth Expenses

Courses, certifications, networking, and business development are investments in future income. Flexibility means recognizing growth expenses as valuable.

5. Adapt to Economic Conditions

Markets rise and fall, inflation changes spending habits. A flexible investor adjusts strategy instead of panicking.

What Are Financial Obligations for Discipline?

Financial obligations are the non-negotiable pillars that protect your future. These are the areas where discipline matters most.

1. Emergency Fund

Maintain at least 6–12 months of essential expenses in liquid savings.

2. Insurance Protection

Health insurance, life insurance, and asset protection are responsibilities, not optional luxuries.

3. Timely EMI & Debt Payments

Missing payments damages credit health and creates unnecessary stress.

4. Monthly Investing Habit

Even small SIPs or recurring investments create long-term wealth through consistency.

5. Tax Planning & Compliance

Ignoring taxes can cost far more later. Smart planning avoids penalties and saves money legally.

Flexibility + Discipline = Sustainable Wealth

Think of it this way:

- Discipline builds the foundation

- Flexibility makes the journey enjoyable

- Both together create sustainability

Someone who saves aggressively but burns out may quit entirely.

Someone who enjoys today but ignores tomorrow may regret it later.

The ideal path lies in between.

A Simple Monthly Formula

You may consider dividing income like this:

- 50% Essentials – rent, bills, groceries, obligations

- 20% Investments & Future Goals

- 20% Lifestyle & Personal Enjoyment

- 10% Emergency / Opportunity Fund

(Percentages may vary based on personal circumstances.)

Questions to Ask Yourself Today

- Am I too rigid with money?

- Am I too casual with money?

- Do I have protection for emergencies?

- Do I allow myself healthy enjoyment?

- Is my financial plan practical for real life?

Final Thoughts

Money management should not feel like punishment. It should feel like empowerment.

Create financial resolutions that give you freedom.

Respect financial obligations that create discipline.

When freedom and discipline work together, financial peace becomes possible.